This post has been de-listed

It is no longer included in search results and normal feeds (front page, hot posts, subreddit posts, etc). It remains visible only via the author's post history.

This is my second R1. Constructive criticism is appreciated.

My attention was brought to this article by a user in another thread.

The author, a Ph.D. in history, makes an incredible claim:

Bernanke actively presided over stagflation II.

Now, the first thought that would occur to anyone who knows their economics is “hang on, hasn’t inflation been below target?” The author has the following choice words for you:

Citing the CPI to the contrary is to adduce the weakest evidence in the service of a bad argument.

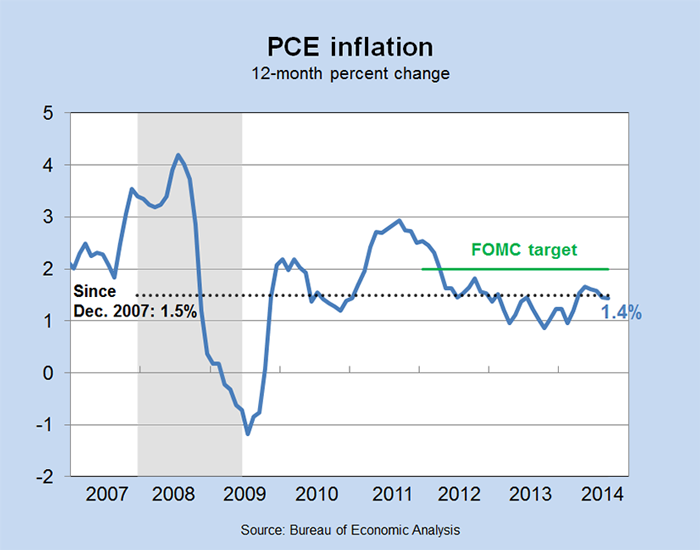

The author also seems to believe that the Fed’s preferred inflation measure is the CPI. We know that the Fed actually prefers the PCE. Some of the reasons as to why the Fed prefers the PCE are explained clearly in that article:

The PCE includes a broader range of expenditures than CPI. It’s weighted according to data provided in business surveys, rather than the less reliable consumer surveys used to weight the CPI. And it uses a formula that adjusts for changes in consumer behavior that occur in the short term, something the standard CPI formula doesn’t do.

As an aside, I'd also note that PCE has been below the Fed's target for well over 30 months now.

{kind=link}

However, one assumes that none of this would sway the author since his article would suggest that all price indices are useless. This apparent stance forces me to ask, how then are we supposed to measure change in prices. The author seems to fall back on a theory of "soundness," whatever that is supposed to mean:

Traditionally, in determining “inflation,” one should balance the CPI against more purely market signals, such as the exchange-rate value of the dollar and the price of gold

There is a lot to unpack in this statement. The assertions made are:

The price of gold is a signal of inflation.

The Dollar's exchange rate is a measure of inflation.

Let us start with the first. Under a fiat currency regime, the price of gold is not reflective of much of anything. A report compiled by the CFA institute in 2013 examined this issue in some detail. A quick glance at Figure 3 reveals a sort of random cloud. There is additional commentary throughout the paper, but, for the sake of briefness, I will quote the following text under Figure 4:

{kind=link}

{kind=link}

What about the ability of gold to hedge, or keep pace with, longer-term inflation? From Figure 4 we can make at least four observations. First, perfect knowledge of the future rate of inflation did not translate into an accurate forecast of future nominal or real gold price returns (inflation did not predict gold returns). Second, knowing future nominal and real gold returns provided no real insight into the course of future inflation (gold returns did not predict inflation). Third, variation in the real price of gold accounted for most of the variation in the nominal price of gold. Finally, given that the trailing 10-year real gold return was negative from 1988 to 2005, it is obvious that gold might have failed to live up to investor expectations as an effective long-term inflation hedge. [emphasis mine]

The second assertion also falls apart under fairly light scrutiny. The author seems blissfully unaware that the exchange rate value of the dollar has risen by quite a bit since under Bernanke's watch as investors fled to the relative safety of the United States. If a strong exchange rate is the author's preferred measure of low inflation, he should be ecstatic. However, this does not seem to be the case. The people shouting "QE! QE! DEBASER! DEBASER!" were hilariously wrong.

Infact, the exchange rate has risen so much that Fed Governor Lael Brainard famously used the following argument for holding off on a rate hike in a October 2015 speech that was much watched by Fed Watchers:

Over the past year, a feedback loop has transmitted market expectations of policy divergence between the United States and our major trade partners into financial tightening in the U.S. through exchange rate and financial market channels. Thus, even as liftoff is coming into clearer view ahead, by some estimates, the substantial financial tightening that has already taken place has been comparable in its effect to the equivalent of a couple of rate increases.

As an aside, I highly recommend people read the speech and follow the excellent Tim Duy on his Fed Watch blog.

I've already gone on for far too long. In conclusion, I'd like to invoke one of my favourite economists, Arthur Okun, in citing the Misery Index. The more esoteric among you may already know that the Misery Index is just Inflation Unemployment, the magic ingredients of stagflation.

Here is a chart of the misery index from 1950-2015. Take a look at the 1970's to see what stagflation looks like. Then, take a look at the present era.

{kind=link}

No respectable economist can claim that Bernanke gave us stagflation.

Subreddit

Post Details

- Posted

- 8 years ago

- Reddit URL

- View post on reddit.com

- External URL

- reddit.com/r/badeconomic...